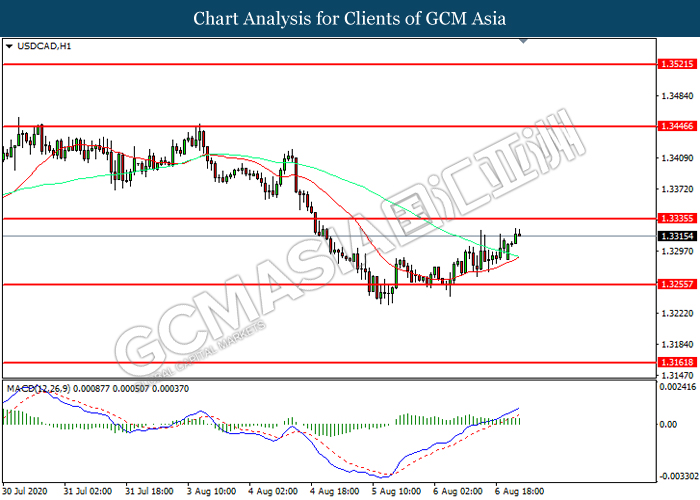

GCMAsia-USDCAD

USDCAD

2020-08-07

USDCAD, H1: USDCAD was traded higher while currently near the resistance level at 1.3335. However, MACD which illustrated diminishing bullish momentum suggest the pair to be traded lower in short-term as technical correction.

Resistance level: 1.3335, 1.3445

Support level: 1.3255, 1.3160